https://www.rousepartners.co.uk/wp-content/uploads/2025/01/UKHospitality-Parliamentary-Reception.jpg

1436

702

Rouse

Rouse

https://www.rousepartners.co.uk/wp-content/uploads/2025/01/UKHospitality-Parliamentary-Reception.jpg

Welcome to our coverage of the highly anticipated Budget announcement, with our team providing key highlights and pinpointing the areas they believe are most significant. We hope that this provides you with useful updates and please contact us if you have any questions on how these affect you.

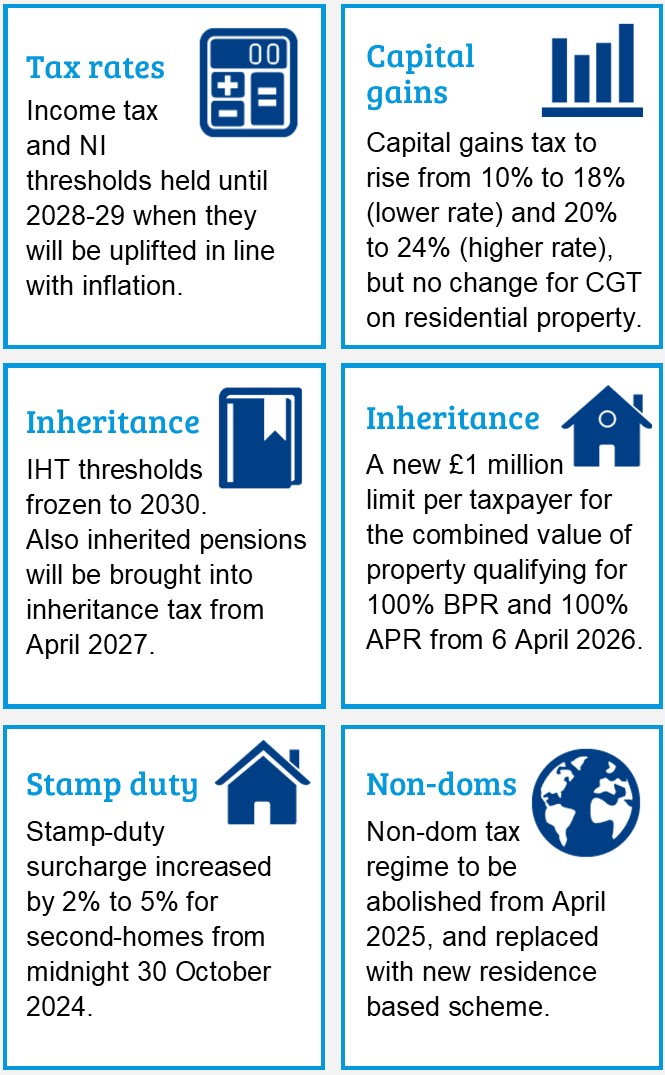

Highlights for individuals

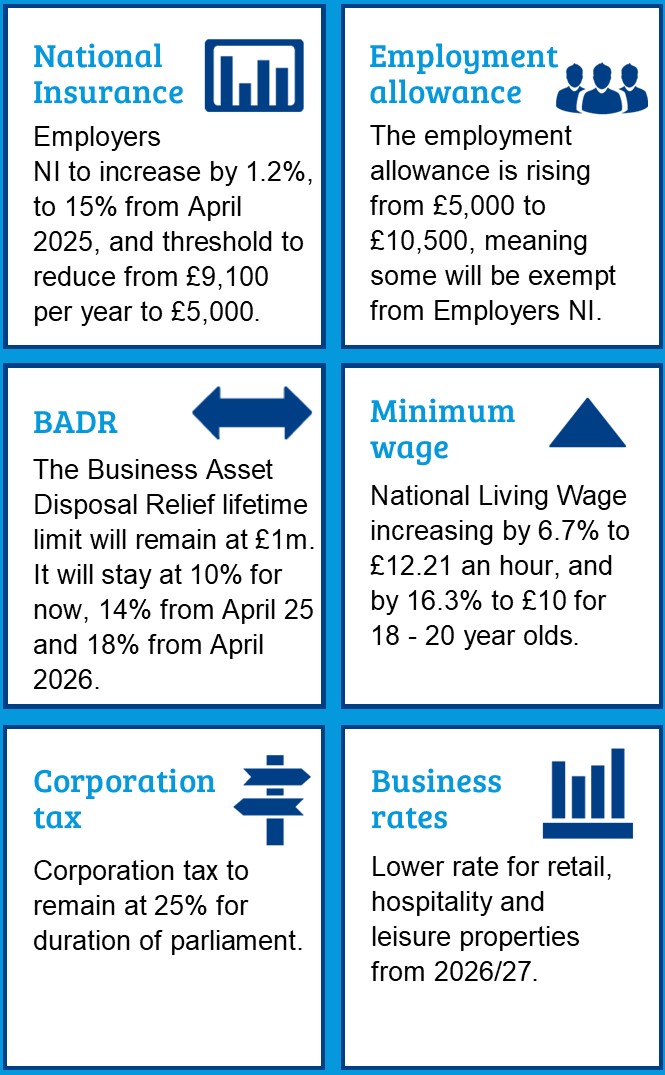

Highlights for businesses

Reaction from our team

Paul Woodward, Director of Tax says:

Paul Woodward, Director of Tax says:

The expected increase in CGT rates was not as significant as feared and the retention of Business Asset Disposal Relief (BADR) is good news for those selling a business. The big downside is the change to Business Property Relief (BPR) for IHT purposes which may lead to IHT bills when family businesses are passed on. From a wider business perspective, the increase in employer’s National Insurance Contributions is unwelcome but many smaller businesses will not feel the hit because of the increase in the Employment Allowance.

Jim Thomson, Assistant Tax Manager says:

Jim Thomson, Assistant Tax Manager says:

As widely expected, the existing non-dom regime will be scrapped from April 2025 and replaced with a new residence-based regime. However, there will be some concessions, with the extension to the temporary repatriation facility, which will allow non-doms to bring their historic income and gains to the UK at a reduced rate of tax. The non-dom rule changes will also impact inheritance tax, with worldwide assets being brought into UK IHT for individuals and trusts. An individual is long-term resident (and in scope for IHT on their non-UK assets) when they have been resident in the UK for at least 10 out of the last 20 tax years and then remain in scope for between 3 and 10 years after leaving the UK (subject to transitional points). We will need to see further details that the Government releases to assess the full impact for non-doms.

Rachael Bonner, Personal Tax Manager says:

Rachael Bonner, Personal Tax Manager says:

The extended freezing of the IHT thresholds to 2030 is a blow and will pull more families into IHT, however we are pleased there was no reduction or scrapping of the nil rate band, which had been rumoured. The biggest announcement regarding inheritance tax, on which the Chancellor spent a very short period of time, was that inherited pensions will now be subject to IHT. This could cause people to consider cashing in their pensions in and gifting earlier. Adding pension pots to inheritance tax calculations could also mean more are pulled into losing some of their residence nil rate band, which is gradually removed on estates worth more than £2 million.

Oscar Wingham, Tax Partner says:

Oscar Wingham, Tax Partner says:

The changes to APR and BPR are a major problem for farming families and family-owned trading companies. It could mean land must be sold, or businesses broken up, to pay the IHT. Share valuations will be critical and will likely add to the cost and time of managing a deceased estate. No doubt these valuations will also be an area of focus and challenge for HMRC. For businesses, the increase in the main rate of Employer’s National Insurance is expected to have the most immediate impact, particularly alongside rising wage costs. Beyond the headline announcements, the Budget reaffirmed previously made commitments to cap the headline rate of corporation tax and maintain key incentives such as full expensing, the annual investment allowance, R&D tax relief rates, and the Patent Box regime. These measures will provide businesses with much-needed certainty about the future direction.

Related insights

New Fair Payment Code launched: How to apply and protect your business from late payments

https://www.rousepartners.co.uk/wp-content/uploads/2024/10/Late-payment-crack-down.jpg

1920

1280

Rouse

Rouse

https://www.rousepartners.co.uk/wp-content/uploads/2024/10/Late-payment-crack-down.jpg

New Fair Payment Code launched: How to apply and protect your business from late payments

Company size thresholds to change from April: Will it impact your reporting?

https://www.rousepartners.co.uk/wp-content/uploads/2024/10/Company-size-threshold-changes.jpg

1920

1280

Rouse

Rouse

https://www.rousepartners.co.uk/wp-content/uploads/2024/10/Company-size-threshold-changes.jpg